Everyone in tokenized finance talks about Ondo. At conferences. On X. On LinkedIn. In pitch decks sent to my inbox at 2am. If you work in real-world assets, Ondo is the name that comes up first and most often.

And for good reason. The platform has real products. Real volume. Real institutional partners that would make any crypto project jealous.

But then I looked at the token, tokenomics, vesting schedule, governance structure. The story everyone tells about Ondo doesn't match what the cap table actually shows.

I have reviewed over 200 tokenized asset projects in the last three years. This is everything I found on Ondo.

The Origin Story

Ondo Finance was founded in 2021 by Nathan Allman, a Brown and Stanford graduate who previously worked in Goldman Sachs' Digital Assets division, alongside Pinku Surana. The pitch: tokenize US Treasuries and money market instruments, make them accessible through crypto wallets. Not vaporware. Actual products.

The early money believed in it. Pantera Capital led a $4 million seed round in August 2021. By April 2022, Founders Fund and Pantera co-led a $20 million Series A. Notably, this was Founders Fund's first-ever token investment. Coinbase Ventures and Digital Currency Group also joined.

That early cap table matters. Because the people who invested $24 million in 2021-2022 are now sitting on tokens in a protocol with $3.5 billion in TVL. Understanding who they are and what they hold is the entire point of this article.

What Ondo Actually Builds

First, what works. There's a lot to parse here.

USDY (Ondo US Dollar Yield)

USDY is a yield-bearing dollar token backed by short-term US Treasuries. Currently $720 million in TVL. Pays 3.55% APY. Available on Ethereum, Polygon, Solana, and XRP Ledger. Minimum investment: $5,000.

The mechanics are simple: you deposit dollars, Ondo buys Treasuries, you earn the yield. The token represents your claim. Daily dividend distributions.

One critical detail: USDY is not offered to US persons. If you're American, you can't buy it. Ondo structured it this way to dodge SEC registration. That's important.

OUSG (Ondo Short-Term US Treasuries)

OUSG tokenizes short-term US government bonds. $666 million in TVL. 3.44% APY. This is Ondo's institutional product. Qualified purchasers and accredited investors only.

The key connection: OUSG is backed primarily by BlackRock's BUIDL fund. Ondo is the single largest recipient of BUIDL's TVL, receiving approximately 42% of BUIDL's growth. Recently paid $1.7 million in monthly dividends to holders.

This is real money, real yield from real Treasuries. No DeFi magic. No reward emissions subsidizing returns. Government bonds wrapped for crypto access.

Ondo Global Markets

Launched September 2025. Over 200 tokenized stocks available: Apple, Tesla, Nvidia, the usual names. Surpassed $500 million in TVL by January 2026. In partnership with Chainlink for price feeds, and distributed through Gate.io, Talos, and Binance.

The claim: 58% market share in tokenized stocks. I have not independently verified this, but even if directionally accurate, it is significant. Ondo is the dominant player in a category that barely existed 18 months ago.

Ondo Chain

Announced February 2025. Launched February 2026. A permissioned Layer-1 blockchain built on Cosmos SDK with proof-of-stake consensus. Validators are selected financial institutions and asset managers. Not anyone. Selected.

Designed as the first permissioned L1 for regulated RWA trading. Compliance sits at the protocol level. Banks get what they actually need: legal sign-off without death by committee.

The Numbers That Matter

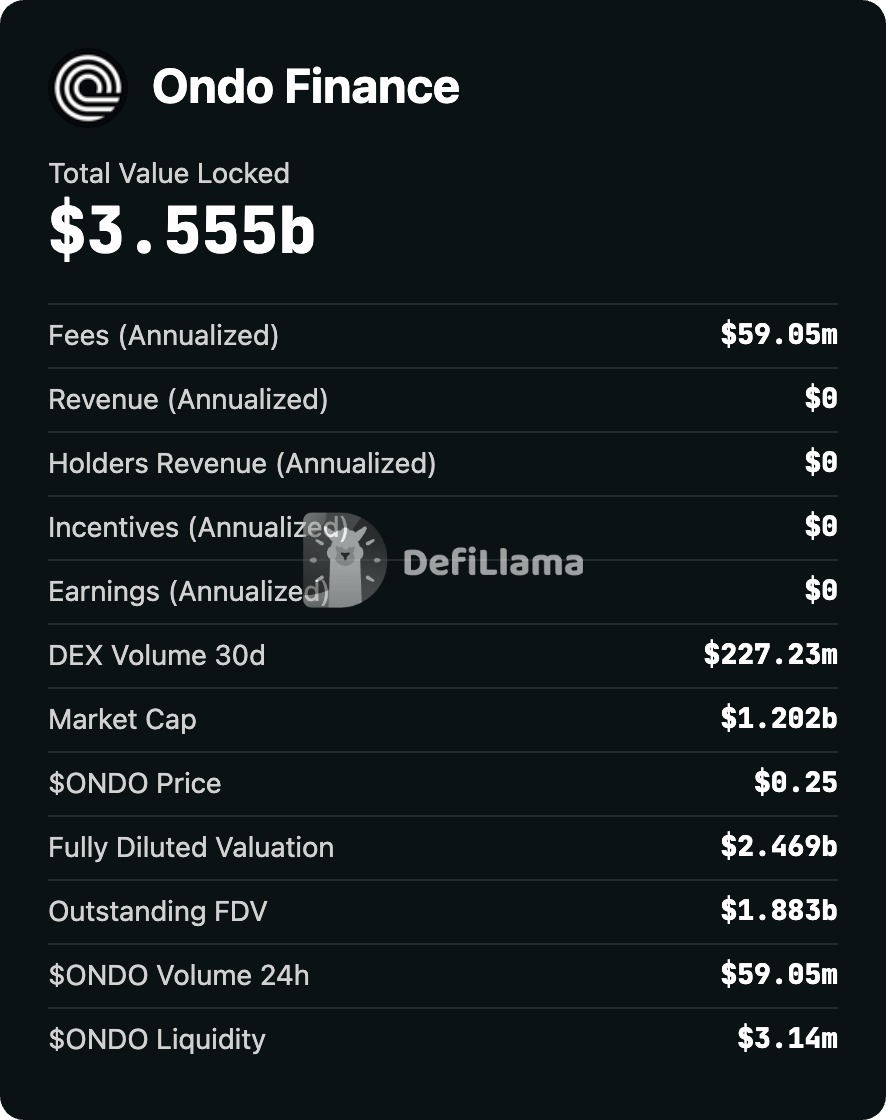

$3.555 billion in total TVL across all products as of April 2026. The platform generates $59 million in annualized fees. 188,000+ token holders. The sector's tokenized assets passed $27.6 billion, and Ondo represents the single largest slice.

Ondo's TVL ($3.55B) is three times its market cap ($1.22B). Market cap/TVL ratio: 0.34. The platform keeps growing. The token keeps tanking.

The partnerships are not just logos on a slide deck:

BlackRock: BUIDL integration powers OUSG. $1.9 billion fund. The world's largest tokenized fund.

Franklin Templeton ($1.7 trillion AUM): Tokenizing versions of its ETFs. Five ETFs went live through Ondo in March 2026. Accessible 24/7 via crypto wallets. Initially rolling out in Europe, Asia, the Middle East, and Latin America.

State Street + Galaxy Digital: Co-created the SWEEP fund. Ondo committed $200 million in seed capital. A tokenized money market/liquidity fund launching on Solana with expansion to Stellar.

ABN Amro: RWA issuance infrastructure partnership. Aon: Risk management for institutional investors. Ripple: OUSG expansion to XRP Ledger.

These are not handshake announcements at conferences. These are production integrations with some of the largest financial institutions on the planet.

The 98% Problem

The other side looks different.

ONDO has a total supply of 10 billion tokens. Here is who holds what:

Read those numbers again. 98% of all ONDO tokens are controlled by insiders, the Foundation, and early investors. The community sale distributed tokens to approximately 18,000 investors. Everyone else, every retail buyer on Binance or Gate.io, is trading within a 2% sliver.

Currently 4.86 billion tokens are in circulation (out of 10 billion total supply). The rest is vesting. In January 2026, 1.94 billion tokens unlocked at once. That is 19% of total supply. More unlocks are scheduled for January 2027 and January 2028, each releasing roughly 1.7 billion tokens.

Every one of those events is potential sell pressure from people who acquired their tokens at seed-round prices or as team compensation. Their cost basis is a fraction of current market prices.

What Does the Token Actually Do?

Governance. That's it.

ONDO holders vote on protocol proposals. In theory, you shape the direction. In practice, 85% of supply sits with the Foundation and team, so your vote means almost nothing.

Let me list what ONDO does not do:

- No staking. You cannot stake ONDO for rewards.

- No gas usage. Ondo Chain has its own fee mechanism. ONDO is not the gas token.

- No revenue sharing. The platform generates real revenue from its products. None flows to token holders.

- No dividends. USDY and OUSG generate yield for their holders. ONDO holders get nothing.

- No buybacks. No mechanism to reduce supply based on platform performance.

- No burn mechanism. Unlike Canton's burn-mint equilibrium, ONDO has no deflationary pressure tied to usage.

The platform makes money. Token holders see none of it.

Compare this to Canton Network (my previous roast), which at least has a burn mechanism where fees paid in CC get burned, creating some connection between network activity and token value. ONDO does not even have that.

The platform already generates $59 million in annualized fees and $13.26 million in quarterly revenue (Q1 2026). Token Holder Net Income: $0. Ondo says fee distribution to token holders is coming in the second half of 2026. No details. No timeline. No commitment.

The BlackRock Halo Effect

The market's interpretation of BlackRock doesn't match reality.

BlackRock created BUIDL, a tokenized money market fund. It crossed $1.9 billion in assets. It is the world's largest tokenized fund. Impressive.

Ondo's OUSG product invests primarily in BUIDL. That means Ondo is a distributor and customer of BlackRock's product. Ondo buys BUIDL and wraps it for crypto-native access.

That is legitimate and useful. But it is not "BlackRock backs Ondo" in the way the market seems to interpret it. BlackRock has a product. Ondo distributes it. The way a wealth management firm might distribute Vanguard ETFs to its clients. Nobody says "Vanguard backs my wealth manager."

Larry Fink's 2026 letter mentioned tokenization 40+ times. He compared it to "where the internet was in 1996." BlackRock cites $150 billion in assets connected to digital markets. This is real institutional commitment to the tokenization thesis.

But BlackRock's commitment is to BUIDL and to the tokenization infrastructure. Not to the ONDO token. BlackRock wins regardless of whether ONDO trades at $2 or $0.02. Their interest is in fees from BUIDL, not in your token price.

The Franklin Templeton and State Street partnerships are more direct. But the same logic applies: these institutions benefit from Ondo the platform. They have zero economic interest in Ondo the token.

The Price Disconnect

ONDO is trading at $0.25 (down 71% YoY). Market cap: $1.22B. Fully diluted: $2.51B. ATH: $1.70. That's an 85% drawdown on a project with $3.5B TVL, $1.7T-AUM partners, $59M annual fees, $13.26M quarterly revenue.

The market cracked the code: platform success doesn't drive token price if the token has no claim on anything.

TVL can triple. Revenue can start flowing. Franklin Templeton can tokenize every ETF in their catalog. And none of it mechanically drives ONDO price up. Because the token has no claim on any of it.

The only way ONDO appreciates is if future demand for the token exceeds the constant supply pressure from vesting unlocks. And with 5.14 billion tokens still locked and scheduled to hit the market over the next two years, that is a steep hill.

The January 2026 unlock of 1.94 billion tokens coincided with the price collapsing further from already-depressed levels. Two more unlocks of similar size are coming. The math is not kind to late entrants.

Competitor Landscape

How does Ondo compare to others in the space?

Securitize: More regulated, legacy infrastructure focus. Lower TVL. But they issued BlackRock's BUIDL directly, so they sit upstream of Ondo in the value chain. Interesting power dynamic.

Centrifuge: Real-world asset financing. More decentralized philosophy. Smaller scale. Different niche (credit, not Treasuries).

Backed Finance: European focus. Tokenized securities on-chain. Smaller partnerships. Regulatory advantage in EU.

Maple Finance: Lending protocol. Different category entirely, though often grouped with RWA.

Ondo's advantage: highest TVL, strongest institutional partnerships, broadest product suite (yield tokens, stocks, dedicated chain). In terms of pure traction, nobody else is close.

The question is whether that traction translates to token value. So far, the market says no.

Security and Audits

Ondo has been audited by EtherAuthority, Quantstamp, and Certik. Smart contracts are certified. An active bug bounty program runs on Immunefi.

No major security incidents or exploits have been reported as of April 2026. For a protocol handling $3.5 billion, this is significant. Institutional-grade security appears to be a genuine priority, not just a marketing claim.

My Verdict: The Same Four Questions

I use the same framework for every project.

1. Does the yield survive real math?

The platform products (USDY, OUSG) deliver real yield from real US Treasuries. 3.44-3.55% APY. No DeFi ponzinomics. No emission-subsidized yields. This is as real as it gets in crypto.

But zero yield flows to ONDO token holders. The platform is profitable. The token is not.

2. What do you actually own?

A governance token with ceremonial voting power in a protocol where 85% of supply is controlled by the Foundation and team. No revenue share. No staking. No gas utility. No burn mechanism.

You own ceremonial voting rights in a protocol where the insiders already decided everything.

3. Can you actually exit?

Better liquidity than Canton. ONDO trades on major exchanges (Binance, Gate.io). But with 5.14 billion tokens still vesting and three major unlock cliffs ahead (one already past, two more in 2027 and 2028), every rally faces a potential wall of insider selling.

Liquidity exists. Whether it exists at your entry price when you need it is a different question.

4. Skin in the game?

The institutions are deeply committed. BlackRock, Franklin Templeton, State Street. Real capital. Real integration. Real products.

But their skin is in the platform infrastructure and the fee revenue. Not in the ONDO token. They win whether ONDO goes to $10 or to $0. Their economic interest is structurally disconnected from yours.

The Bottom Line

Ondo Finance is probably the most important infrastructure project in tokenized finance today. The technology works. The partnerships are real. The TVL is real. The products deliver real yield from real assets.

If Ondo were a private company offering equity, I would tell serious investors to take a hard look. The team has executed at a level almost nobody else in RWA has matched.

But Ondo is not offering you equity. It is offering you a governance token with:

- No revenue share

- No staking

- No burn mechanism

- 98% insider concentration

- Years of unlocks creating constant sell pressure

- Zero mechanical connection between platform success and token price

The platform and the token live in parallel universes. One is thriving. The other is down 85% from all-time highs.

That's not coincidence. That's the market doing math you should do too.

I work in this space. I review these projects because I believe in what tokenization can do. But believing in the technology does not mean buying every token associated with it. Sometimes the best way to participate in a revolution is to invest in the infrastructure, not in the merchandise.

Sources and Data

- CoinMarketCap: ONDO

- DeFiLlama: Ondo Finance TVL

- Tokenomist: ONDO Vesting Schedule

- CryptoRank: ONDO Token Unlocks

- BlackRock: Larry Fink 2026 Chairman's Letter

- Ondo Foundation Docs: The ONDO Token

- Ondo Finance Official

- Congress Tokenization Hearing, March 25 2026

Frequently asked questions

What is Ondo Finance and what does it actually build?

Ondo Finance was founded in 2021 by Nathan Allman, a former Goldman Sachs Digital Assets analyst, and Pinku Surana. It builds four real products: USDY (yield-bearing dollar token, $720M TVL, 3.55% APY, not offered to US persons), OUSG (tokenized short-term US Treasuries, $666M TVL, 3.44% APY, qualified purchasers only, backed primarily by BlackRock's BUIDL fund), Ondo Global Markets (200+ tokenized stocks including Apple, Tesla, Nvidia; claimed 58% market share in tokenized equities), and Ondo Chain (a permissioned Layer-1 launched February 2026 with selected financial-institution validators).

How much TVL does Ondo Finance have and what is the relationship to its token market cap?

Ondo's total platform TVL was $3.555 billion across all products as of April 2026, generating roughly $59 million in annualized fees and serving more than 188,000 token holders. The ONDO token market cap was around $1.22 billion at the same time. That puts the market-cap-to-TVL ratio at roughly 0.34. The platform keeps growing; the token price has not kept pace.

Why is 98% of the ONDO token supply controlled by insiders?

Out of a 10 billion total supply, 52.1% sits with the Ecosystem Growth / Foundation / DAO, 33% with Protocol Development and the team, 12.9% with private-sale investors, and 2% with the community via the CoinList sale (roughly 18,000 retail investors). That means 98% of all ONDO tokens are controlled by insiders, the foundation, and early backers. Every retail buyer on Binance or Gate.io is trading within a 2% float.

What is Ondo's relationship with BlackRock?

OUSG, Ondo's institutional tokenized-Treasury product, is backed primarily by BlackRock's BUIDL fund — the world's largest tokenized fund, with about $1.9 billion AUM. Ondo is the single largest recipient of BUIDL's TVL, receiving roughly 42% of BUIDL's growth. Recent monthly dividends to OUSG holders were approximately $1.7 million.

Can US persons buy USDY?

No. USDY is explicitly not offered to US persons. Ondo structured the product this way to avoid SEC registration. American investors cannot buy USDY, regardless of accreditation status.

Who are Ondo's institutional partners and are they real or slide-deck?

Production integrations rather than handshake announcements: BlackRock (BUIDL powers OUSG), Franklin Templeton ($1.7T AUM, five tokenized ETFs live through Ondo as of March 2026), State Street + Galaxy Digital (co-created the SWEEP fund with Ondo committing $200M in seed capital), ABN Amro (RWA issuance infrastructure), Aon (institutional risk management), and Ripple (USDY expansion to XRP Ledger). Ondo Global Markets distributes through Gate.io, Talos, and Binance with Chainlink as price-feed oracle.