Circle fell about 14% on June 30, and touched down 16% intraday, on the launch of a stablecoin that has never moved a single dollar.

Sit with that for a second, because it is the whole story. Open USD has no live volume, no firm launch date, nothing that settles yet. Circle dropped anyway. That tells you the market was not pricing in lost market share. It was pricing in what this design does to Circle's margins. The 140 logos everyone is posting about are the least interesting thing here. We will get to why.

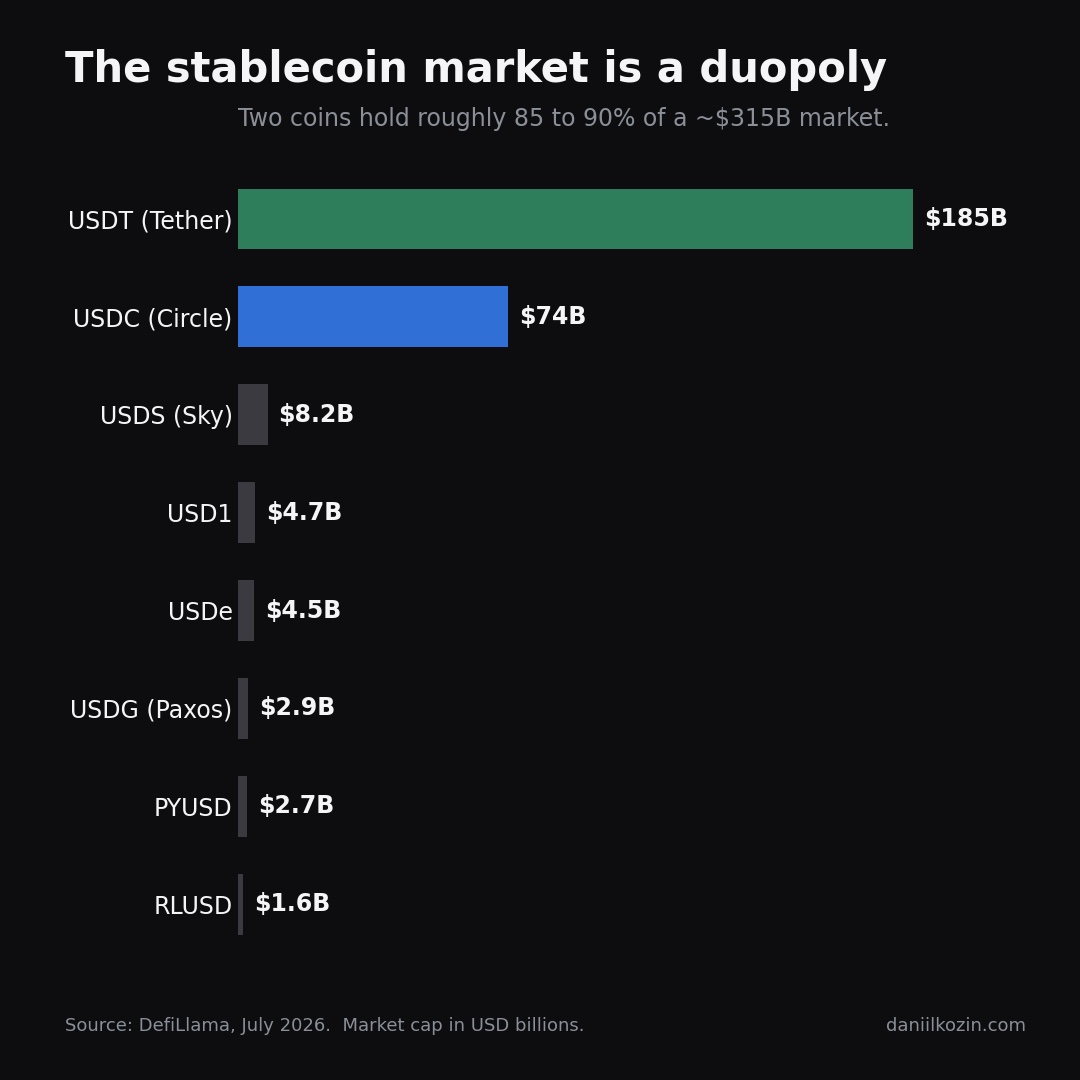

The market, by the numbers (the part everyone skips)

Before the drama, the map. The total stablecoin market sits around $315 billion (DefiLlama and the Fed's April note bracket it at $313 to $317B). It grew from roughly $135B at the end of 2023 to over $300B by the end of 2025. 2026 so far is a plateau, not a surge.

And it is not a crowded field at the top. It is a duopoly.

- Tether (USDT): about $185 billion, roughly 59% of the market.

- Circle (USDC): about $74 billion, roughly 24%.

- Everyone else is a rounding error by comparison: Sky Dollar (USDS) ~$8B, World Liberty's USD1 ~$4.7B, Ethena's USDe ~$4.5B, Paxos's consortium coin USDG ~$2.9B, PayPal's PYUSD ~$2.7B, Ripple's RLUSD ~$1.6B.

Two names hold roughly 85 to 90% of the entire market. That number has barely moved despite years of well-funded attempts to break it. That is the fact that should frame everything you read about Open USD today.

One more number, because it cuts through the hype in both directions. Stablecoins settled somewhere between $33 and $35 trillion in 2025. Sounds world-eating. But by most estimates only about 1% of that was real-world payments. The rest is trading, arbitrage, and bots moving money between venues. The "stablecoins are eating payments" story is mostly still a story. Keep that in your pocket for the Open USD pitch.

Why the two kings actually stay kings

New entrants keep assuming the incumbents win on brand or luck. They win on physics.

Liquidity begets liquidity. Market makers keep their inventory where the pairs are deepest and the fees are best, which is USDT and USDC, which makes those pairs deeper, which pulls in more market makers. It is a flywheel, and flywheels are brutally hard to stop from the outside.

Exchanges are the kingmakers. USDC is what it is largely because Coinbase made it the default. USDT is what it is because it had a four-year head start building trading-pair depth nobody else has. You do not win that by announcing a better design. You win it by grinding distribution for years.

And now there is a regulatory moat too. The GENIUS Act, signed into law in July 2025, is the first real US federal framework for stablecoins: full 1:1 backing, short-dated Treasuries, monthly reserve disclosures, audits. It legitimized the incumbents and raised the floor for everyone else. It also did one specific thing that matters enormously for today's story: it banned issuers from paying holders any yield. Remember that. It is the hinge the whole Open USD design swings on.

The graveyard is instructive. In 2019 Facebook lined up the exact same kind of logo wall for Libra, later Diem: Visa, Mastercard, PayPal, Stripe, eBay, Vodafone. Every name you would want. Regulators saw a Facebook-run world currency, moved to kill it, the marquee partners walked within months, and it was wound down by 2022, its assets sold for scraps. And a closer, quieter precedent: Paxos already runs a shared-yield consortium coin, the Global Dollar Network, live since late 2024 with Robinhood, Kraken and Galaxy. Its design is basically what Open USD is proposing. Nearly two years in, it has reached about $2.9 billion, against USDC's $74 billion. A consortium and a better yield split, and it is a rounding error. That is your base rate.

So what is Open USD, really

Give it its due first, because this is not Diem and it is not a scam.

Open USD is a dollar stablecoin from a new company called Open Standard, governed collectively by its partner businesses rather than a single issuer, modeled on the Paxos network above. Its founding CEO is Zach Abrams, who co-founded Bridge, the stablecoin infrastructure company Stripe bought in 2024. The pedigree is real. More than 140 companies have signed on, and the list is genuinely absurd in the best way: Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, Google, Shopify, American Express, Fiserv, Klarna, IBM, DoorDash, Samsung, a wall of banks, and most of the major chains. It goes live on Solana first, "later this year."

Now the honest part. The list is the cheapest thing to assemble in a consortium launch and the worst predictor of whether the thing ships. Diem had this exact wall. So 140 logos does not read as a moat. It reads as a hedge. Most of these companies are buying cheap insurance against a rival owning the neutral settlement rail. That is a very different thing from committing real volume to it.

You can see the hedge most clearly in the members who already shipped their own coins. Western Union, Fiserv, SoFi and MoneyGram all launched stablecoins of their own this past year, and they are on this list anyway. That is not a contradiction, it is a portfolio. Their own coin stays for the closed loop where they keep everything. Open USD is the layer they plug into to settle with the outside world, and it lets them earn yield instead of paying an issuer for the privilege. Rational. Also shallow, until Open USD actually has liquidity, which today is zero.

The float is the real target

Here is the decision that actually moved the stock, and it has nothing to do with logos.

Circle's entire business is the float. It takes the dollars backing USDC, parks them in short-term Treasuries, and keeps the interest. That is not a side line. Reserve income is roughly 96 to 99% of Circle's revenue. The company essentially is a rate trade wrapped in a token. This is the same lesson the verifiable-revenue guide draws about the whole category: the money is in who captures the yield, and here Circle captures all of it.

Open USD hands that yield back to the partners, minus a thin management fee. And because the GENIUS Act forbids paying yield to holders, routing it to business partners is the only legal way to weaponize it. Read that as a pricing attack, not a feature. Even if Open USD never takes a dollar of share from USDC, it resets what a large business expects to earn for holding a stablecoin. The moment "the issuer keeps your float" stops being the default, Circle's margin is under pressure on the volume it already has.

The pressure point is even sharper than it looks. Coinbase takes 100% of the reserve interest on USDC held on its platform, and splits the rest with Circle 50/50. That arrangement is worth around $900 million a year and is reportedly up for renewal around August 2026. Coinbase is on the Open USD partner list. You do not need a conspiracy chart to see the leverage in that.

That, not some volume migration next year, is why Circle dropped.

USDC is not dead, though

The panic is overdone in the other direction too. USDC is about $74 billion, live and regulated across dozens of chains, and wired into things that are hard to rip out: BNY custody, institutional settlement, real payment rails Circle has spent years building (its own network, cross-chain transfer, an on-chain FX stack). CEO Jeremy Allaire shrugged the announcement off: "USDC remains the most trusted, widely adopted stablecoin globally."

Open USD, by contrast, has a press release and zero live volume until later this year. The boring regulatory and integration grind that actually wins distribution, Circle has a multi-year head start on. The threat to Circle is margin compression, not a sudden exodus. Those are very different things, and the market conflated them for a day.

Who funds a free stablecoin?

There is also a hole inside Open USD's own design that none of the launch quotes address. If mint and redeem are free, and essentially all the yield goes to partners, who funds the thing that actually wins payments? Distribution is bought with incentives, integrations and business-development spend. SWIFT can run as a thin cooperative because it has fifty years of lock-in. A day-one stablecoin has none. Open USD needs scale to fund growth and growth to get scale, and it is starting that loop with a deliberately skinny middle. The consortium is the answer to "who pays." But a consortium of a hundred rivals is exactly where roadmaps go to die. Ask anyone who sat through Diem governance, or watched a bank consortium take years to ship what one company would have built in months.

The odds, and the honest verdict

My read: this is a serious attempt, the yield mechanic is genuinely smart, and the part everyone is celebrating, the breadth, is the part I would worry about. The bigger the tent, the slower the decisions and the shallower each member's commitment. Rob Hadick at Dragonfly put it well: the partners suggest a real threat, but consortiums are hard and they break easily, because the incentives are broad and often misaligned.

It is too early to draw a conclusion, and anyone telling you Circle is finished is selling you certainty that does not exist yet. The base rate says consortium yield-sharing coins struggle to move the incumbents. The design says the margin attack is real regardless.

So do not watch the logo count. Watch two numbers.

First, live Open USD volume six months after it launches. Intent is free. Settlement is not. If in mid-2027 it is still a press release with a wallet attached, the market answered the question.

Second, and more important, watch what Circle does to its own economics. If Circle quietly starts sharing reserve yield to defend its biggest accounts, then Open USD has already won the only fight that was ever really on, without moving a dollar of volume. The stock did not fall because 140 companies signed a list. It fell because the price of holding a stablecoin just changed, and Circle's whole business is on the other side of that price.

This is analysis, not investment advice. All figures are as of July 1, 2026 and should be verified on neutral sources before any decision. I hold no position in Circle or any token mentioned.

Frequently Asked Questions

Why did Circle (CRCL) stock drop on the Open USD launch?

It fell about 14% (roughly 16% intraday) on June 30, 2026, on a stablecoin with zero live volume. The market was not pricing in lost share; it was pricing in the hit to Circle's margins. Circle's revenue is roughly 96 to 99% reserve income on the Treasuries backing USDC, and Open USD hands that yield to partners instead. That resets what a business expects to earn for holding a stablecoin, pressuring Circle's margin on the volume it already has.

What is Open USD (OUSD)?

A consortium dollar stablecoin from Open Standard, governed by its partner businesses, led on an interim basis by Zach Abrams (Bridge co-founder). 140+ partners including Visa, Mastercard, Stripe, BlackRock, Coinbase, and Google. Free mint and redeem, reserve yield shared with partners less a management fee, Solana first, later in 2026. Zero live volume at announcement.

Will Open USD kill USDC?

Too early to say, and probably not soon. USDC is ~$74B, live, regulated, and deeply integrated. The base rate is discouraging for the challenger: Paxos's shared-yield consortium coin (USDG) is only ~$2.9B nearly two years in. The realistic threat to Circle is margin compression, not a sudden exodus.

How does Circle make money?

The float. It parks the dollars backing USDC in short-term Treasuries and keeps the interest, roughly 96 to 99% of revenue. The sharpest pressure point is the Coinbase deal (reportedly ~$900M/yr, up for renewal ~August 2026); Coinbase is on the Open USD list.

What is the GENIUS Act's yield ban?

The GENIUS Act (US law, July 2025) requires 1:1 backing, Treasuries, disclosures, and audits, and bans paying yield to stablecoin holders. Routing yield to business partners instead is the only legal way to weaponize it, which is exactly Open USD's design. The yield reaches partners, not holders.

Why do USDT and USDC dominate?

Liquidity, exchange distribution, and a multi-year grind, not coin design. Two names hold ~85 to 90% of a ~$315B market, and that share has barely moved despite years of funded attempts. A better design announced at launch does not overcome the flywheel quickly.

What should I watch next?

Two numbers, not the logos: live Open USD volume six months after launch, and whether Circle starts quietly sharing reserve yield to defend its accounts (watch the Coinbase renewal ~August 2026). If Circle shares yield, Open USD already won without moving a dollar.

Daniil Kozin structures tokenized real-asset deals in Europe and writes the analysis series to watch the number, not the narrative. The stablecoin market is the tokenized-cash corner of the same RWA story; the tokenized-treasury side is covered in the BUIDL vs BENJI vs USDY vs USDM guide, and the "who captures the yield" question runs through the whole archive.

Disclaimer: This is analysis, not investment advice. Figures are as of July 1, 2026 and should be verified on neutral sources. The 140-name roster and the "all yield to partners" economics are, at this stage, self-reported from a launch with no live product; treat the partners as signed to a list, not as committed volume. The Coinbase deal value and renewal timing are largely single-source and framed as reported. I hold no position in Circle or any token mentioned.

Sources:

- CoinDesk: Circle slides as Stripe, Coinbase and BlackRock back rival stablecoin network (30 Jun 2026)

- CoinDesk: why Open USD's real threat still faces a steep uphill battle for adoption (30 Jun 2026)

- DefiLlama: total stablecoin market cap ~$313B; USDT ~$185B (59%), USDC ~$74B (24%), USDG ~$2.9B, PYUSD ~$2.7B, RLUSD ~$1.6B (July 2026).

- Circle USDC transparency page (~$73.7B circulation, 29 Jun 2026) and Circle FY2025 results (reserve income ~96% of revenue).

- White House / Congress.gov: GENIUS Act signed 18 Jul 2025, including the issuer yield ban.

- Decrypt / USDC.org: Coinbase reserve-interest split (reportedly ~$900M/yr, renewal ~Aug 2026).

- CoinDesk / Bloomberg: Libra/Diem history (wound down Jan 2022); Rob Hadick (Dragonfly) on consortium fragility.

- Bloomberg / Artemis: 2025 stablecoin settlement volume ~$33 to $35T, of which ~1% real-world payments.

Data and relationships as of July 1, 2026. Verify current figures on neutral sources before any decision.