Plume raised from Brevan Howard. It became the first blockchain the SEC registered as a transfer agent for tokenized securities. It put real institutional names on its cap table and a real regulatory first on the board.

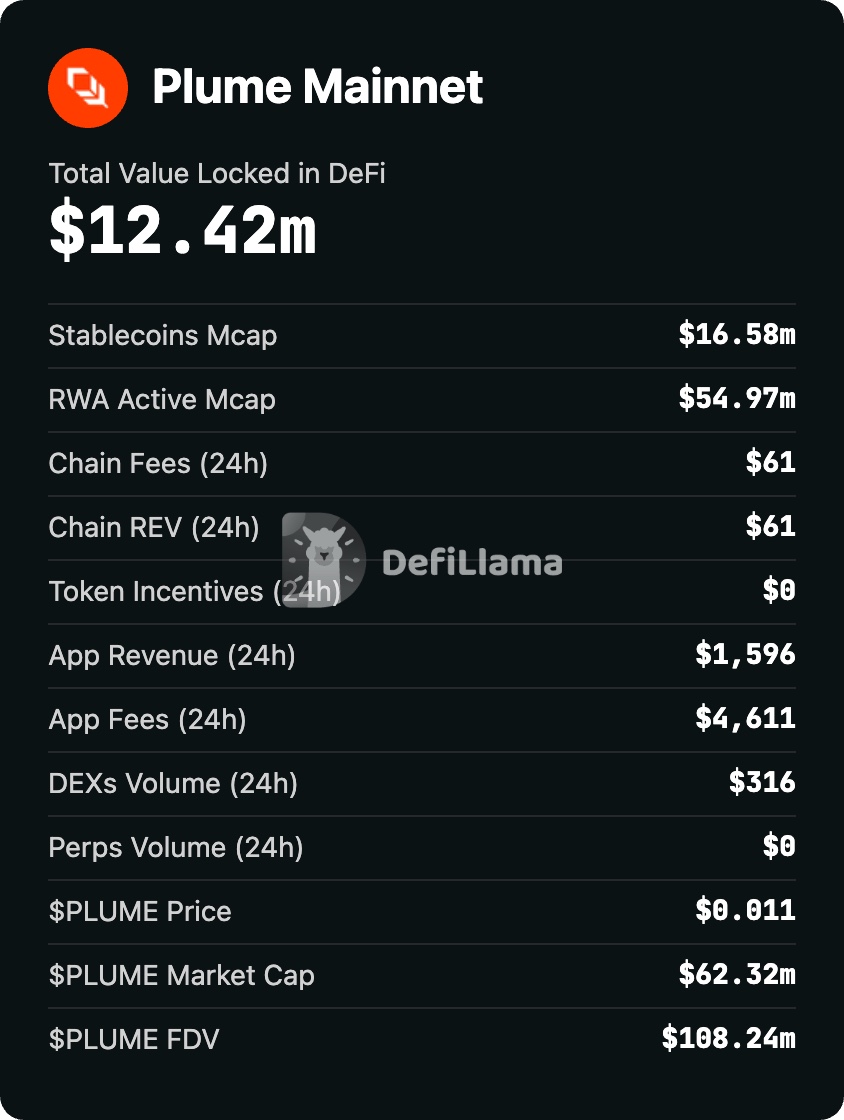

Today its chain earns 61 dollars a day in fees and holds 12 million dollars in total value, down from roughly 300 million at its peak.

Both of those sentences are true at the same time. That gap is the entire roast.

What Plume Actually Is

Plume is an EVM-compatible chain built specifically for real-world asset tokenization. Genesis mainnet went live on June 5, 2025, after a 2024 testnet. The native token, PLUME, handles gas, staking, and governance. The branding is "RWAfi": real-world assets plus DeFi composability on one chain tuned for both.

The pitch has three parts. A chain with gas optimised for the operations RWA tokens use, like compliant transfers and registry updates. A curated set of protocols built for tokenized collateral and yield. And a bridge layer to pull tokenized assets in from Ethereum and other chains.

One honest note on the basics: even Plume's own architecture description has shifted. Early materials called it a "fully integrated modular Layer 1." Later coverage and its own posts describe a modular Layer 2. For an allocator that distinction matters for where settlement and security actually live, so check current documentation rather than the funding-round press release.

The Team

Plume was founded in January 2024 by three people: Chris Yin (CEO), Teddy Pornprinya (CBO), and Eugene Shen (CTO). Yin is a repeat founder. Shen came from an engineering background, including time as a software engineer at Robinhood, and led the technical build.

In May 2025, Eugene Shen died suddenly. The company announced it at the end of that month. I am noting it because an honest team assessment cannot pretend a chain lost its technical co-founder and nothing changed. This is said with respect for a person, not as a mark against anyone: losing a founding CTO this early is a real loss and a real continuity question, and it belongs in any serious read of the project. Chris Yin and Teddy Pornprinya continue to lead.

The investor base is the most-cited credibility signal, and it is genuine. Haun Ventures led the 10 million dollar seed in May 2024. Brevan Howard Digital led the 20 million dollar Series A in December 2024, with Haun, Galaxy Ventures, and Lightspeed Faction alongside. In April 2025, Apollo Global Management made a strategic investment. Roughly 30 million dollars is disclosed, with additional undisclosed strategic capital on top.

Two corrections worth stating plainly, because backing claims get repeated until they become fact. The widely-circulated "around 50 million across rounds" figure is not confirmed by any disclosed round; treat it as an estimate, not a number. And Polychain, which shows up in some write-ups as a Plume backer, does not appear in any of Plume's funding rounds. It is not an investor here.

Cap-table quality is necessary but not sufficient. Polymesh had institutional backing. MANTRA had Laser Digital and family offices, and collapsed anyway. Backing has never predicted which dedicated RWA chains capture share.

The Regulatory First That Actually Matters

This is the part the conference slides get right, and it is real.

On October 6, 2025, Plume became an SEC-registered transfer agent for tokenized securities. In plain terms, that lets it maintain shareholder records, process transfers, and handle distributions on-chain, while linking cap tables and reporting into the SEC and DTCC systems. Plume has said it is pursuing ATS and broker-dealer registrations next. The token jumped about 30 percent the day it was announced.

No other dedicated RWA chain has this. Polymesh, Centrifuge, Provenance, and the rest have compliance architecture, but not a live transfer-agent registration that plugs into the existing securities plumbing. If the thesis behind Plume survives, this is the piece most likely to be the reason. It moves Plume from "another chain" to "a chain that can legally sit inside the regulated securities workflow."

So credit where it is due. On the regulatory axis, Plume is ahead of its category. For how this compares to the platform-side regulatory stacks, see the Tokeny vs Polymath vs Securitize vs Centrifuge comparison.

The Numbers: What the Chain Actually Does Today

Here is where the story turns, and it turns hard. These figures are from DefiLlama and rwa.xyz as of mid-June 2026.

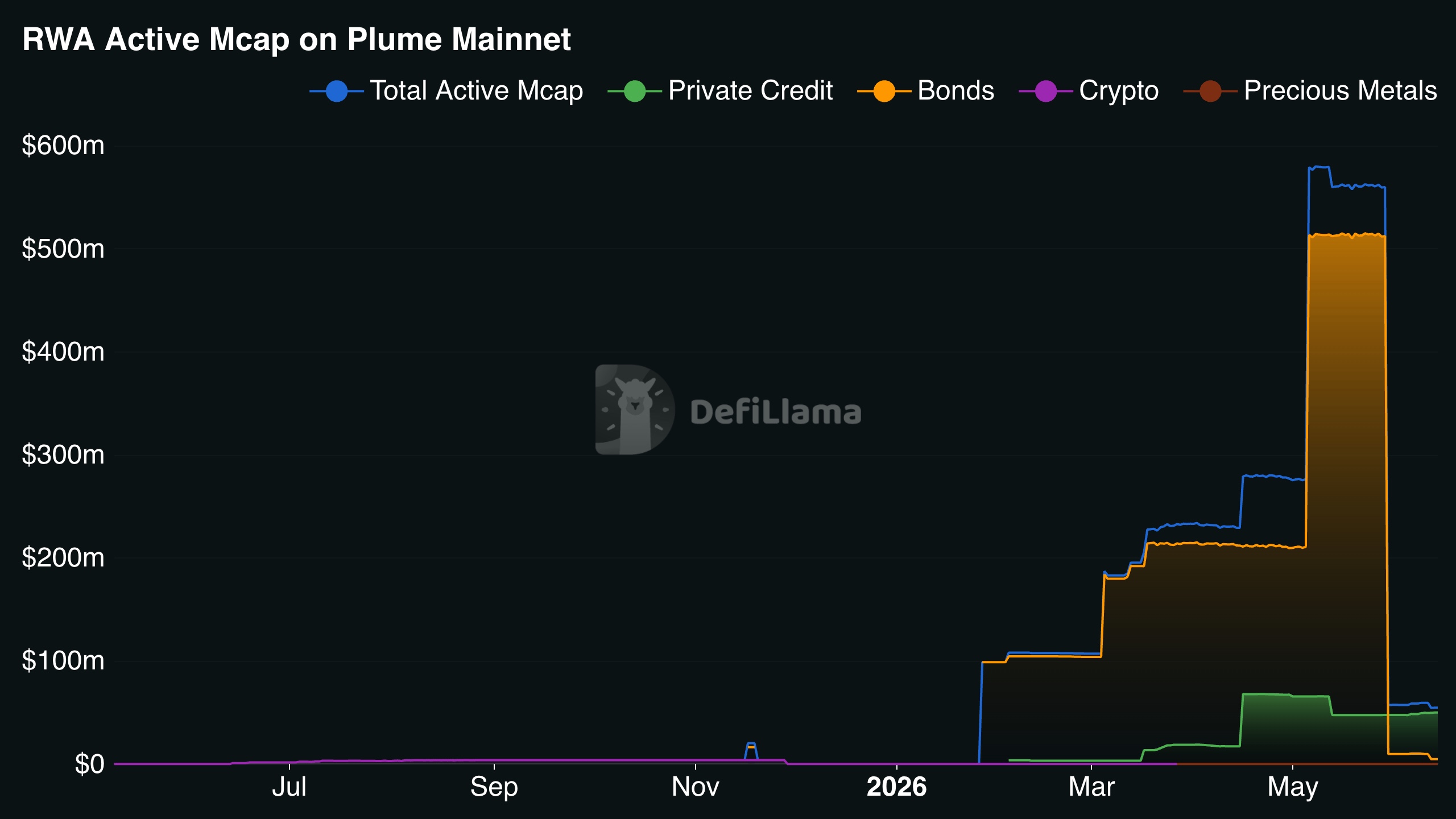

Total value locked in DeFi on Plume: about 12.4 million dollars. At its peak around October 2025 it was roughly 300 million. It held near 150 to 160 million into the end of 2025, then fell off a cliff at the start of 2026.

Tokenized real-world asset value on the chain ran up to roughly 600 million dollars by May 2026, mostly bonds, then collapsed to about 55 million by mid-June. Stablecoins on the chain sit around 16.6 million.

Chain fees over 24 hours: 61 dollars. App revenue over 24 hours: about 1,600 dollars. For a chain whose entire pitch is being the optimised home for RWA-specific operations, 61 dollars a day in fees is the number that should stop you. The activity that was supposed to justify a dedicated chain is not there right now.

Two things drove the cliff. First, the January 20, 2026 token unlock released about 1.37 billion PLUME, roughly 39.75 percent of circulating supply, into the market. Second, whatever pushed RWA value to 600 million in spring 2026 left almost as fast as it arrived, which is the signature of incentive-driven or rotational capital rather than sticky institutional allocation.

The Token

PLUME has a 10 billion max supply and handles gas, staking, and governance. It trades around 0.011 dollars, a market cap near 62 million, and a fully-diluted valuation near 108 million. Its all-time high was around 0.25 dollars. That is a decline of roughly 95 percent from the high.

The pattern here is the one that recurs across dedicated RWA chains: the protocol can do real things while the token captures almost none of it. Centrifuge processed over a billion dollars in tokenized credit, and CFG never reflected it. Polymesh trades thin. MANTRA's OM was destroyed. Provenance has real loan volume and HASH has never been a category-defining asset. The detailed version of that pattern is in the Centrifuge Roast.

For PLUME specifically, the structural questions are unforgiving right now. Fully-diluted value near 108 million against chain fees of 61 dollars a day. A 39.75 percent supply unlock already in the market. Staking rewards that, at this fee level, are emissions rather than earned revenue. Before sizing any position, the question is not whether the chain succeeds. It is whether the token would capture it even if it did.

What Plume Gets Right

Three things deserve credit regardless of the chart.

The SEC transfer-agent registration is real and category-leading. This is the genuine differentiator, and it is not marketing.

The cap table is real. Brevan Howard Digital, Haun, Galaxy Ventures, Lightspeed Faction, and an Apollo strategic check are not tourists. The institutional interest in the category is sincere.

The thesis is coherent. A dedicated chain with native compliance, tuned gas, a curated ecosystem, and DeFi composability is a defensible architecture. It may not be the bet that wins. It is not an obviously bad one.

The "RWAfi" Branding

RWAfi means tokenized assets should plug into lending, borrowing, and yield rather than sit on chain as static entries. Plume brands itself as the chain optimised for it.

Two honest qualifiers. This is not new: Centrifuge fed tokenized credit into MakerDAO years ago, and Ondo, Maple, and Aave have run versions of asset-plus-DeFi for a long time. And branded chain categories have a mixed record. "DePIN" launched a wave of projects in 2024, most of which delivered nothing. Evaluate on substance, not the label.

The Scorecard

| Category | Score | Notes |

|---|---|---|

| Team | 5/10 | Real founders and backers. Lost co-founder/CTO Eugene Shen suddenly in 2025; genuine continuity risk. |

| Funding / cap table | 7/10 | Brevan Howard, Haun, Galaxy Ventures, Lightspeed, Apollo strategic. ~$30M disclosed. "$50M+" unverified; Polychain is not an investor. |

| Thesis (RWAfi) | 6/10 | Coherent, not novel. Category has produced no winner. |

| Technical architecture | 6/10 | EVM-compatible; L1-vs-L2 self-description has shifted. Bridge layer adds complexity. |

| Regulatory positioning | 8/10 | SEC-registered transfer agent (Oct 2025), pursuing ATS and broker-dealer. Category-leading and real. |

| Ecosystem traction | 3/10 | TVL ~$12.4M (from ~$300M peak). RWA value ~$55M (from ~$600M in May). Chain fees $61/24h. |

| Token economics | 3/10 | ~95% below ATH. 39.75% supply unlock in Jan 2026. Fees negligible vs $108M FDV. |

| Transparency | 5/10 | Public team, funding, and docs. Architecture described inconsistently. Verify all metrics on DefiLlama/rwa.xyz. |

| Overall | 4.8/10 | Best regulatory credential in the category, worst current on-chain trajectory. Weighted toward what an allocator faces today, not the round. |

The Four Questions

Does the yield survive real math? Not applicable to a chain directly. It applies to assets issued on Plume (their own underlying yield) and to PLUME staking, where at 61 dollars of daily chain fees, staking rewards are emissions, not earned revenue. Be clear which one you are being sold.

What do you actually own? Two layers. PLUME holders own a chain token with gas and governance utility and a 95 percent drawdown. Holders of RWA tokens issued on Plume own whatever the issuer's legal wrapper says, with Plume as the technology layer, not the legal structure. The chain adds technology and bridge risk on top of asset risk.

Can you actually exit? PLUME, yes, on exchanges, at a price that has fallen 95 percent. For assets issued on Plume, exit depends on the token's own secondary market and on whether Plume's curated DeFi has the depth, which at 12 million dollars of TVL it currently does not, or whether bridging back to Ethereum stays the real exit.

Skin in the game? Institutional, given the cap table. But a 39.75 percent supply unlock has already hit the market in January 2026, which tells you how much of the early alignment has now been freed to sell. Verify remaining vesting before reading the cap table as long-term alignment.

The Bottom Line

Plume is the clearest example in the category of the distance between institutional credibility and on-chain reality. The SEC transfer-agent registration is the best regulatory credential any dedicated RWA chain has earned, and it is real. The cap table is real. The team is diminished by a genuine tragedy and still operating.

And the chain today holds 12 million dollars, earns 61 dollars a day, trades 95 percent below its high, and just absorbed a 40 percent supply unlock. The 600 million dollars of tokenized value that arrived in spring left almost as fast, which is what rotational capital looks like, not what an institutional base looks like.

If you are looking at Plume, separate the two stories. The regulatory infrastructure could matter for years. The token, on current numbers, is a speculation on whether activity ever shows up to match the credentials. Judge any asset issued on Plume on the asset and the issuer, never on the chain branding. And size any PLUME position against 61 dollars a day, not against the logos in the round.

Real team, real money, real regulatory first. The verdict is no longer open. On today's numbers it reads as a chain whose credibility is running well ahead of its chain.

I hold no PLUME or Plume-issued tokens. This is not investment advice. Do your own research.

Frequently Asked Questions

What is Plume Network?

An EVM-compatible blockchain for RWA tokenization with DeFi composability ("RWAfi"). Genesis mainnet June 5, 2025. Native token PLUME.

Who is behind Plume?

Co-founders Chris Yin (CEO) and Teddy Pornprinya (CBO). Co-founder and CTO Eugene Shen died suddenly in May 2025. Investors: Haun Ventures (seed lead), Brevan Howard Digital (Series A lead), Galaxy Ventures, Lightspeed Faction, and an Apollo Global Management strategic investment. ~$30M disclosed.

Is Plume SEC-regulated?

Plume became an SEC-registered transfer agent for tokenized securities on October 6, 2025, and has said it is pursuing ATS and broker-dealer registrations. This is service-level registration, not chain-level regulation, and it is currently unique among dedicated RWA chains.

What happened to the PLUME token?

It trades around $0.011, roughly 95% below its all-time high near $0.25. A token unlock of about 39.75% of circulating supply hit the market on January 20, 2026.

What is Plume's on-chain traction?

As of mid-June 2026: TVL around $12.4M (down from a ~$300M peak), tokenized RWA value around $55M (down from ~$600M in May), chain fees around $61/24h. Verify live on DefiLlama and rwa.xyz.

How does Plume compare to Centrifuge?

Different architecture and stage. Centrifuge focuses on tokenized credit with real institutional partners. Plume is a newer EVM chain targeting broad RWA categories with a regulatory edge (transfer agent) but a collapsed on-chain footprint.

Should I buy PLUME?

This is not investment advice. Dedicated RWA chain tokens have a poor track record (CFG, POLYX, HASH, OM). At $61/day in chain fees against a ~$108M FDV, evaluate whether activity can ever match the valuation before sizing anything.

Daniil Kozin structures tokenized real-asset deals in Europe and writes the RWA Roast series to cut through the conference slides. Previous roasts: Justoken, Reental, GromaCoin, Centrifuge, Chainlink, Figure, Stellar, Kelp DAO, Syrup, Ondo, Canton. Full archive at daniilkozin.com/blog.

Disclaimer: I do not hold PLUME tokens or any Plume-issued tokens. This is not investment advice. Do your own research.

Sources:

- Plume Network official site and blog (incl. SEC transfer-agent announcement, tokenomics)

- CoinDesk: Series A ($20M, Dec 2024), Genesis mainnet (Jun 5, 2025), SEC transfer-agent registration (Oct 6, 2025)

- PR Newswire / Fortune: $20M Series A investor list

- Apollo strategic investment coverage (Apr 2025)

- Multiple outlets (Protos, BeInCrypto, Invezz, Coinomist): passing of co-founder Eugene Shen (May 2025)

- Gate / Tokenomist: Jan 20, 2026 unlock (~39.75% of circulating supply)

- DefiLlama: TVL, RWA value, fees, token metrics (as of June 15, 2026; screenshots on file)

- rwa.xyz: tokenized RWA value on Plume

- CoinGecko: PLUME price and ATH

Data as of June 15, 2026. The RWA chain landscape moves fast. Verify live metrics through neutral sources before any commercial decision.