Most people in DeFi lending know the name Maple. Or at least they used to. The protocol lost $54 million in bad debt during the 2022 collapse, watched its TVL crater from $900 million to under $50 million, and seemed finished.

Then the team did something unusual. They rebuilt. Rebranded the retail side as Syrup. Migrated the token from MPL to SYRUP. Pivoted from uncollateralized lending to overcollateralized institutional loans. And by early 2026, they had climbed back to $4.6 billion in assets under management.

That is a legitimate comeback story. But comeback stories make for dangerous investments when you stop reading at the headline.

I ran this project through AI detective swarms that cross-reference on-chain data, legal filings, governance proposals, and tokenomics against the marketing narrative. Here is what the data actually says.

The Origin Story

Sid Powell and Joe Flanagan founded Maple in 2019 with a premise that made sense on paper: bring institutional-grade credit markets on-chain. Let qualified borrowers access DeFi liquidity. Let DeFi depositors earn real lending yields instead of farming unsustainable token emissions.

Powell came from debt capital markets. He had participated in over $3 billion of corporate bond issuance and managed treasury at a commercial lending fintech. That background matters because it suggests the team understood credit risk at a structural level. What happened next suggests they understood it in theory better than in practice.

Maple launched in May 2021. Early backers included Polychain Capital, Framework Ventures, and Paradigm. Total raised: roughly $6.4 million across three rounds, with the latest being a $5 million strategic round in August 2023 led by BlockTower Capital and Tioga Capital. Cherry Ventures, GSR, and Spartan Capital also participated.

The pitch attracted real capital fast. By early 2022, Maple had nearly $900 million in active loans. The team had built a protocol that actually worked for what it was: a marketplace connecting institutional borrowers with DeFi lenders through delegate-managed lending pools.

The problem was what "delegate-managed" actually meant when the delegates stopped managing.

The $54 Million Lesson

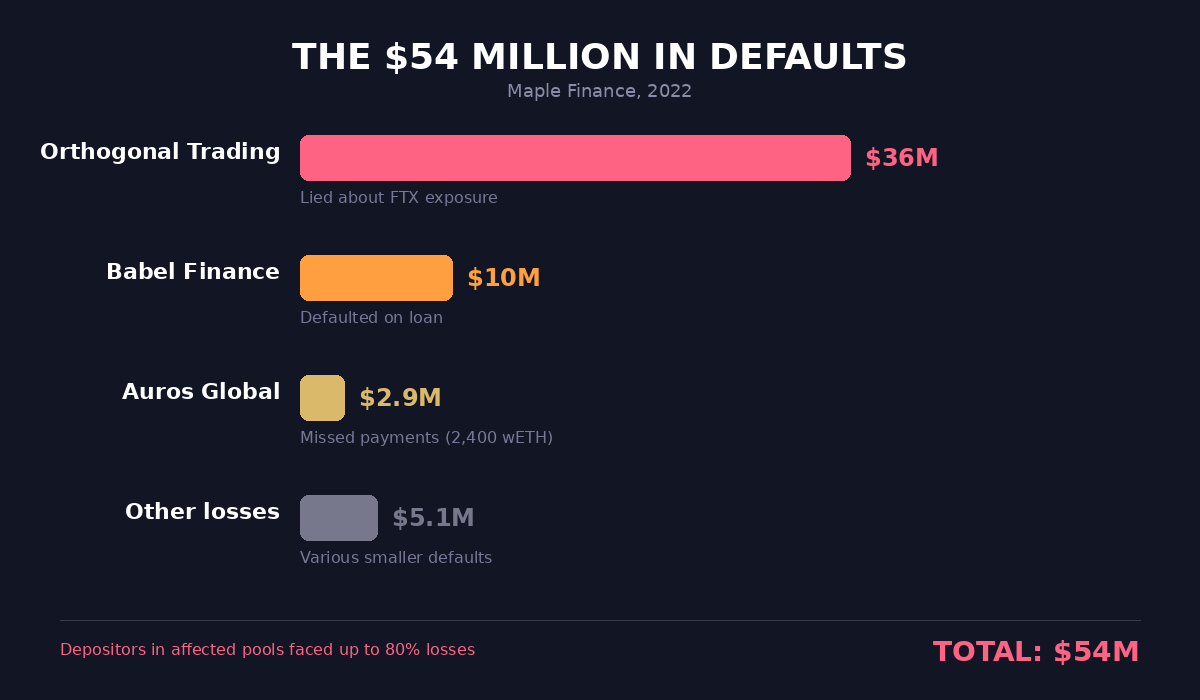

In December 2022, Maple Finance experienced the kind of failure that kills protocols.

Orthogonal Trading defaulted on eight loans totaling $36 million. That was 30% of all active loans on the platform. The reason: Orthogonal had lied about its exposure to FTX. Through November 2022, the firm told Maple's pool delegate M11 Credit that it had "minor exposure" to the collapsed exchange. On December 3rd, Orthogonal admitted the truth. The money was gone.

But Orthogonal was not the only problem.

Babel Finance had already defaulted on a $10 million loan earlier that year. Creditors absorbed $7.9 million in losses. Auros Global missed payments on 2,400 wETH worth $2.9 million. In total, Maple saw $54 million in bad debt. Depositors in the affected pools faced up to 80% losses.

Let those numbers settle. Eighty percent losses. On a lending protocol that marketed itself as institutional-grade.

The root cause was not complicated. Maple's original model was uncollateralized lending. Borrowers went through KYC and were "vetted" by pool delegates, but there was no on-chain collateral backing the loans. When borrowers lied about their financial position, and when the broader crypto market collapsed, there was nothing to liquidate. The deposits were simply gone.

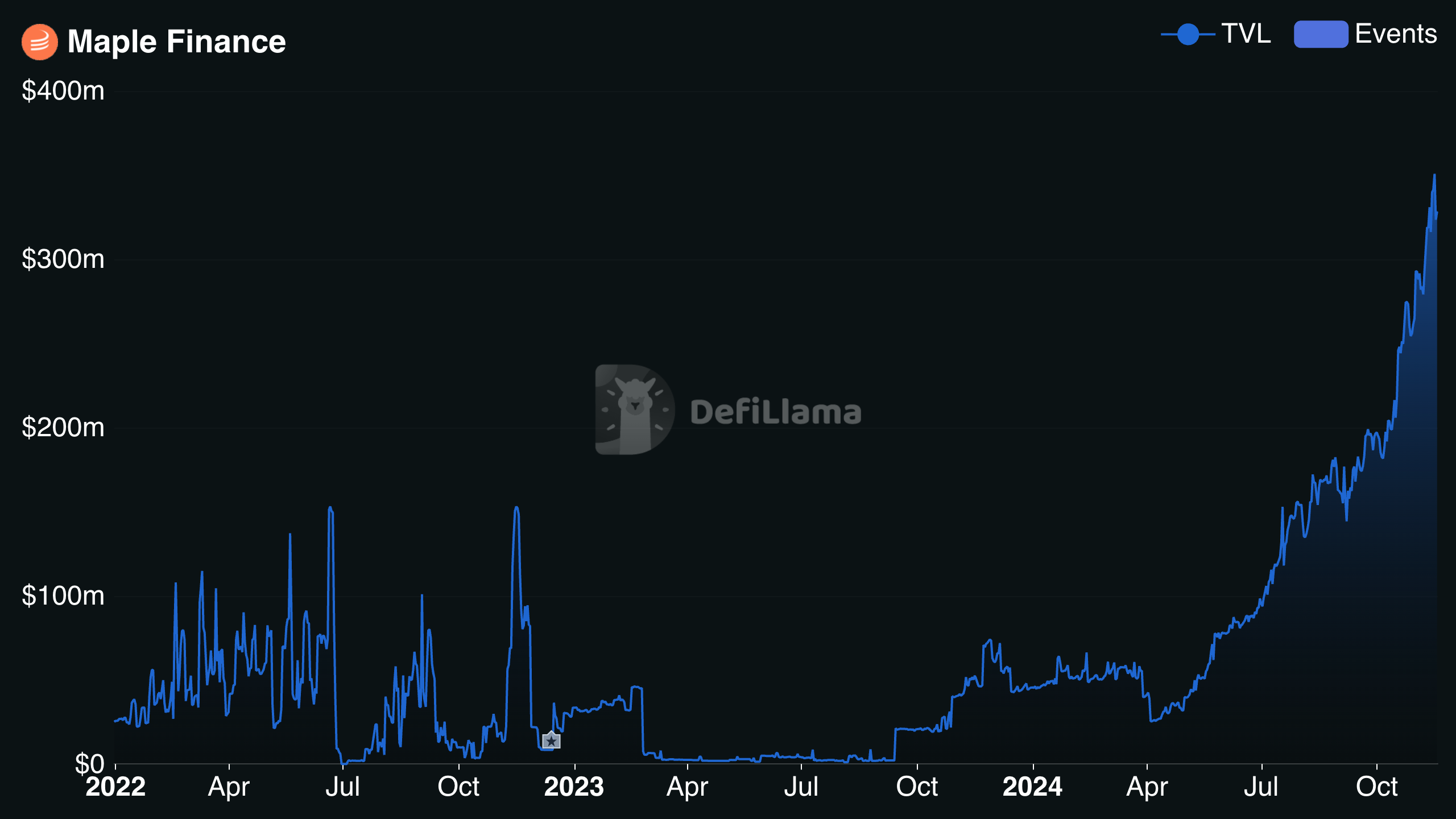

Maple's TVL collapsed from $900 million to $82 million. The protocol nearly died.

The Rebuild: From Maple to Syrup

What happened next is where the story gets interesting, and where most analysis stops too early.

The team rebuilt the protocol from scratch. Maple V2 launched in late 2022 with a critical change: overcollateralized lending only. No more trusting borrowers at their word. Every loan now requires collateral held with institutional custodians like Anchorage, BitGo, and Zodia.

Two main lending pools emerged:

Blue Chip Secured Pool: Accepts BTC and ETH as collateral. Lower yield. Lower risk profile. This is the conservative option.

High Yield Secured Pool: Accepts select digital assets as collateral. Higher yield. Higher risk tolerance. Collateral requirements are still above 100%, with margin calls and liquidation thresholds built into the loan terms.

In June 2024, Maple launched Syrup as the retail-facing arm. Syrup.fi became the front door for non-institutional users. You deposit USDC or USDT, receive syrupUSDC or syrupUSDT as receipt tokens, and earn yield generated from Maple's institutional lending operations.

The numbers on those pools are significant. By December 2025, syrupUSDC and syrupUSDT deposits had crossed $2.2 billion. By early 2026, the combined Maple ecosystem managed roughly $4.6 billion in assets, with each syrup pool exceeding $1 billion individually.

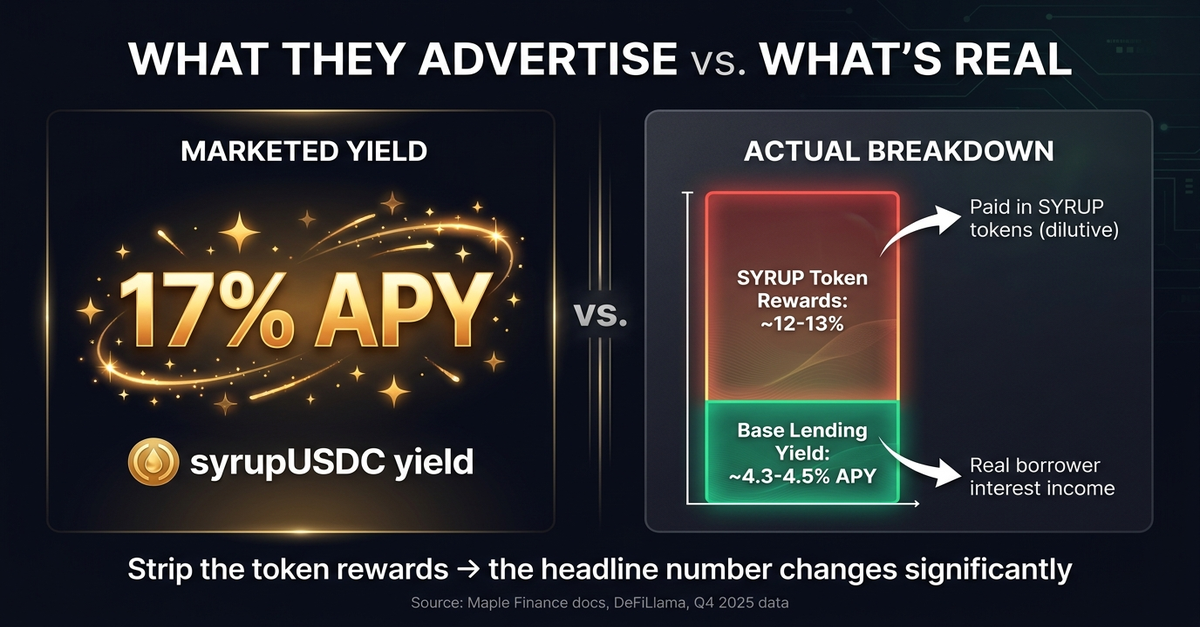

Maple claims 5-10% APY outperformance versus protocols like Aave. At launch, Syrup was quoting 17% APY with a 176% collateral ratio.

That yield has to come from somewhere. Let me show you where.

Follow the Yield

Syrup's yield comes from fixed-rate overcollateralized loans to institutional borrowers. Over 85 institutional borrowers, all KYC/AML verified, borrow through the protocol. The team claims rigorous underwriting and collateral ratios conservatively above 100%.

This is a real business generating real revenue. In Q4 2025, gross protocol revenue reached approximately $30.93 million. That translates to an annualized run rate above $100 million heading into 2026. The team's public target is $100 million in annual recurring revenue by end of 2026.

Monthly revenue hit $2.49 million in October 2025 and has grown since. This is not yield from token emissions. This is interest income from actual lending operations. That distinction matters.

But here is what the marketing leaves out.

When Syrup advertises 17% APY, that figure includes SYRUP token rewards. The base lending yield, the part that comes from actual borrower interest payments, is lower. Maple's "Drips" system distributes ownership tokens to depositors that convert to SYRUP tokens in phases. You can boost rewards with 3-month lockups (1.5x multiplier) or 6-month lockups (3x multiplier).

Sound familiar? Every DeFi protocol that subsidizes yield with its own token eventually faces the same question: what happens when the token rewards dry up or the token price drops? The base yield needs to stand on its own. And at Maple's current fee structure, the base yield to depositors is competitive but not the headline number.

The 17% included token incentives. Strip those out, and you are in a different conversation.

The Token: SYRUP

In November 2024, Maple migrated from MPL to SYRUP at a 1:100 conversion ratio. The initial SYRUP mint was approximately 1.15 billion tokens, composed of:

- 1 billion SYRUP from the base conversion of all MPL tokens

- 100 million from an initial inflation allocation

- ~55 million from accumulated emissions through October 2024

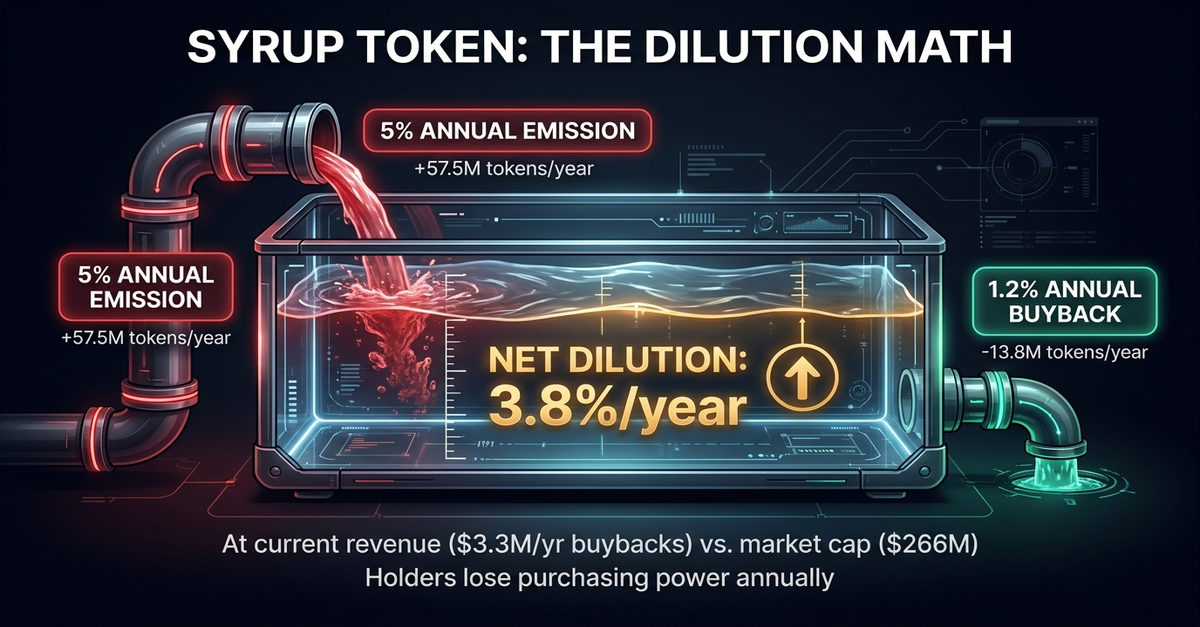

The tokenomics include a 3-year emission schedule at 5% per annum. By September 2026, expected supply will be approximately 1.27 billion SYRUP.

Current circulating supply: roughly 1.16 billion. Market cap: approximately $266 million. Price as of this writing: around $0.22-$0.27, depending on the exchange.

Here is what changed in October 2025, and this is actually notable. Maple governance passed MIP-019 with 91% community support. The proposal ended staking rewards entirely and replaced them with a buyback mechanism. 25% of protocol revenue now flows to a "Syrup Strategic Fund" that buys SYRUP on the open market.

In Q4 2025, that mechanism executed roughly $615,000 in buybacks. In Q1 2026, it grew to $827,000. The team projects this could remove over 2% of SYRUP supply annually if revenue targets hold.

Let me run the math on that. At current prices around $0.25 and a market cap near $266 million, $827,000 quarterly in buybacks means about $3.3 million annually. Against a $266 million market cap, that is 1.2% of market cap in annual buybacks. Not nothing. Not transformative either.

Compare this to the Ondo roast I wrote last month. ONDO has zero buybacks, zero revenue sharing, zero staking, zero burn mechanism. Maple at least has a mechanical connection between protocol revenue and token demand. The buyback exists. Whether it is enough to overcome ongoing token emissions at 5% per year is a math problem that does not resolve in the token holder's favor yet.

5% annual emission. 1.2% annual buyback. Net dilution: roughly 3.8% per year. Your tokens are losing purchasing power annually, and the buyback is not keeping pace.

The Lawsuit Nobody Talks About

In November 2025, the Grand Court of the Cayman Islands granted Core Foundation an injunction against Maple Finance. This is a real legal proceeding, not Twitter drama.

The background: Core Foundation and Maple partnered in early 2025 to develop lstBTC, a liquid Bitcoin staking product. They announced it together in February at an event in Hong Kong. Maple began accumulating client assets through the partnership, reportedly reaching $150 million.

Core alleges that by mid-2025, Maple secretly began developing syrupBTC, a competing product, while still receiving Core's capital, resources, and confidential information. Core claims this violated a 24-month exclusivity agreement and constituted misappropriation of intellectual property.

Judge Jalil Asif found evidence supporting Core's claims that Maple was informed its actions would cause "very significant commercial damage." The injunction blocks Maple from launching syrupBTC or any variants, and from dealing in CORE tokens, pending arbitration.

Maple denied the allegations.

Regardless of who is right, the injunction tells you something about how the team operates under competitive pressure. They had a partner. They had an agreement. And according to the court, there was enough evidence of breach to warrant blocking an entire product launch.

This does not appear in any Maple marketing material. AI detective swarms that scan legal databases found it in five minutes. Your average DeFi depositor never sees it.

Security and Audits

Credit where due: the technical security infrastructure has improved significantly since 2022.

Maple's protocol contracts have undergone audits for the December 2024 release, the September 2025 release, and the November 2025 withdrawal manager upgrade. Auditors include Spearbit and Sherlock. The January 2026 release for CCIP cross-chain deposits was also audited.

No major smart contract exploits have been reported. For a protocol managing $4.6 billion, the technical security record is clean.

But smart contract security and credit risk are different things entirely. The $54 million in defaults was not a hack. The code worked exactly as designed. The humans operating within the system were the point of failure. Overcollateralized loans reduce that risk. They do not eliminate it. A sharp enough market crash can still break collateral ratios before liquidations can execute.

Competitor Landscape

Where does Syrup sit relative to the rest of on-chain credit?

Figure: Larger. Operates more in structured finance. Different niche.

Tradable: Second in tokenized private credit. Lower profile but meaningful volume.

Centrifuge: More decentralized philosophy. First mover in RWA credit. Supports more complex deal types. Smaller scale than Maple's current numbers.

Goldfinch: Focused on emerging market lending. Different risk profile entirely. $100 million in loans. More philosophical alignment with global financial inclusion.

TrueFi: Unsecured lending model. Smaller. Lost momentum after the 2022 credit crunch hit everyone.

Credix: Three-tier default prevention mechanism. More conservative design. Limited participation breadth.

Maple's advantage: highest TVL among pure DeFi credit protocols, strongest revenue generation, most institutional borrowers (85+), and the broadest product suite with syrupUSDC, syrupUSDT, and plans for more syrup assets in 2026.

The disadvantage: Maple is the only major credit protocol in this list that has actually experienced a $54 million default event. That is both a scar and, arguably, a lesson. Whether the lesson stuck depends on how you weight the overcollateralization pivot versus the team's track record of judgment calls.

My Verdict: The Same Four Questions

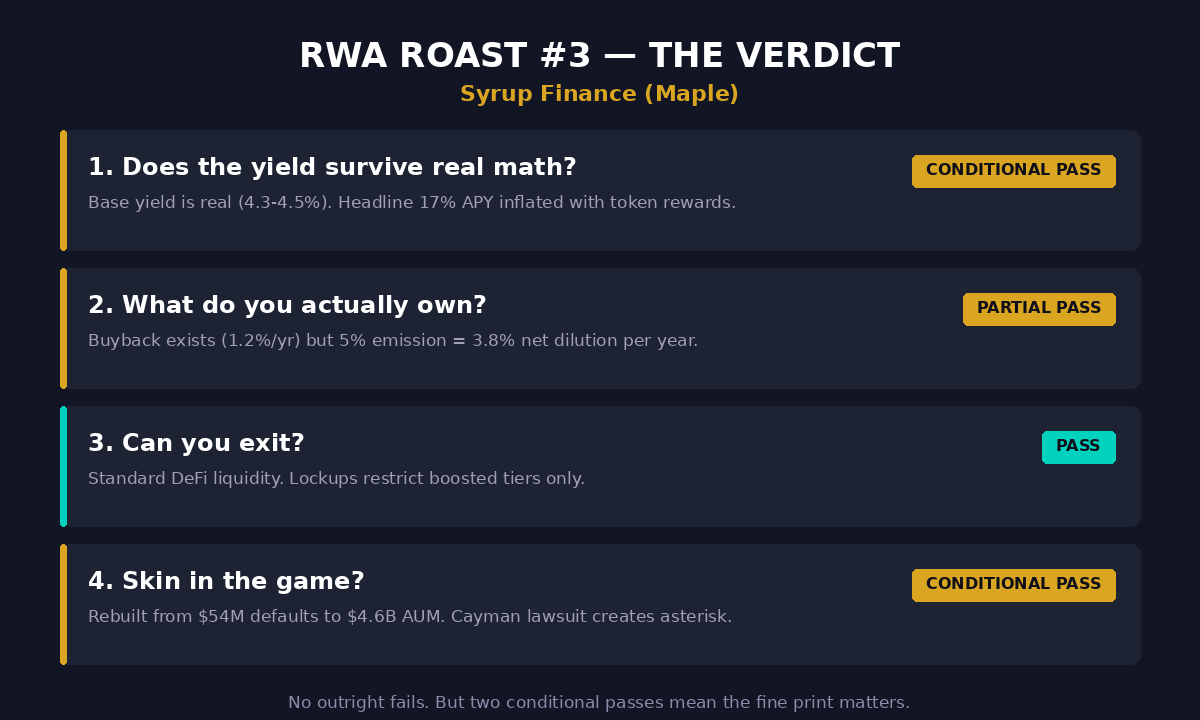

1. Does the yield survive real math?

The base lending yield from institutional borrowers is real. Maple generates genuine interest income from overcollateralized loans. Q4 2025 revenue of $30.93 million is not fabricated.

But the headline APY numbers include SYRUP token rewards that are inherently dilutive. The base yield, stripped of token subsidies, is more modest than the marketing suggests. And the protocol's history includes a $54 million default that wiped out depositors. The model has changed. The team has not.

Conditional pass. The yield is real if you look past the token subsidy layer and accept the residual credit risk.

2. What do you actually own?

SYRUP is a governance token with a buyback mechanism. That buyback is real, funded by 25% of protocol revenue, and executed on a quarterly basis. This is better than Ondo (no buyback, no staking, no revenue connection) and better than Canton (burn mechanism but lower revenue).

But governance remains concentrated. The team and early investors hold significant supply from the MPL-to-SYRUP conversion. Ongoing emissions at 5% per year outpace the buyback by roughly 3:1. You are not being diluted as fast as you would be with pure emission tokens, but you are still being diluted.

Partial pass. Buyback is a real mechanism. Dilution math does not yet favor holders.

3. Can you exit?

SYRUP trades on major exchanges including Coinbase, Binance, and Kraken. Liquidity is reasonable for a $266 million market cap token. The syrupUSDC and syrupUSDT receipt tokens have instant liquidity features the team launched specifically to address redemption concerns.

For depositors: Maple introduced withdrawal manager upgrades in November 2025 to improve the redemption experience. Lockup periods (3-month and 6-month for boosted rewards) do restrict some depositors. If you chase the higher yield tiers, you are locked.

For token holders: standard exchange liquidity. No cliff unlocks the size of Ondo's 1.94 billion token dump, but ongoing 5% annual emissions create steady sell pressure.

Pass for depositors on standard terms. Conditional for boosted yield depositors and token holders.

4. Skin in the game?

Sid Powell has been building Maple since 2019. The team rebuilt after a near-death experience in 2022. They pivoted the entire business model from uncollateralized to overcollateralized lending. They migrated the token. They ended staking when it was not working and replaced it with buybacks. These are decisions that suggest long-term commitment.

But the Core Foundation lawsuit raises questions about how the team navigates partnerships. Allegedly developing a competing product while inside an active exclusivity agreement, if the court's preliminary findings hold, is not a trust-building move. Maple denies it, and the arbitration has not concluded. But the injunction was granted, and the facts the judge cited were specific.

The team also raised only $6.4 million total. That is very lean for a protocol managing $4.6 billion. Either the equity structure has other layers I cannot see, or the team's primary economic interest is in the SYRUP token itself. If the latter, alignment is high. If the former, the picture is incomplete.

Conditional pass. Rebuilding from $54M in defaults shows commitment. The lawsuit creates an asterisk.

The Bottom Line

Syrup Finance is the comeback kid of DeFi lending. The protocol genuinely rebuilt from a catastrophic failure. The overcollateralized model is structurally sounder than the original. Revenue is real and growing. The product works. Eighty-five institutional borrowers are using it. $4.6 billion in AUM is not an illusion.

But the token economics remain unfavorable. 5% annual emissions against 1.2% annual buybacks means holders are diluted net 3.8% per year. The headline APY includes those very emissions. And the protocol's history includes $54 million in depositor losses that no amount of rebranding fully erases.

If you are depositing stablecoins for yield and understand the credit risk, Syrup is competitive. The overcollateralized structure is a genuine improvement. The institutional borrower base is real.

If you are buying the SYRUP token as an investment, the math is harder. The buyback mechanism is a step in the right direction, but it is not yet strong enough to overcome the dilution. Revenue needs to grow substantially, or emissions need to decrease, for the token to work as a standalone investment.

And the Core Foundation lawsuit is a live risk that AI detective swarms flagged but most retail analysis misses entirely. Legal proceedings in the Cayman Islands do not show up in your typical DeFi dashboard. They should.

This is Episode 3 of the RWA Roast series. [Episode 1: Canton Network.] [Episode 2: Ondo Finance.] Episode 4 coming soon.

If you want your project reviewed, DM me.