02 / The breakdown

Every category, with the honest math.

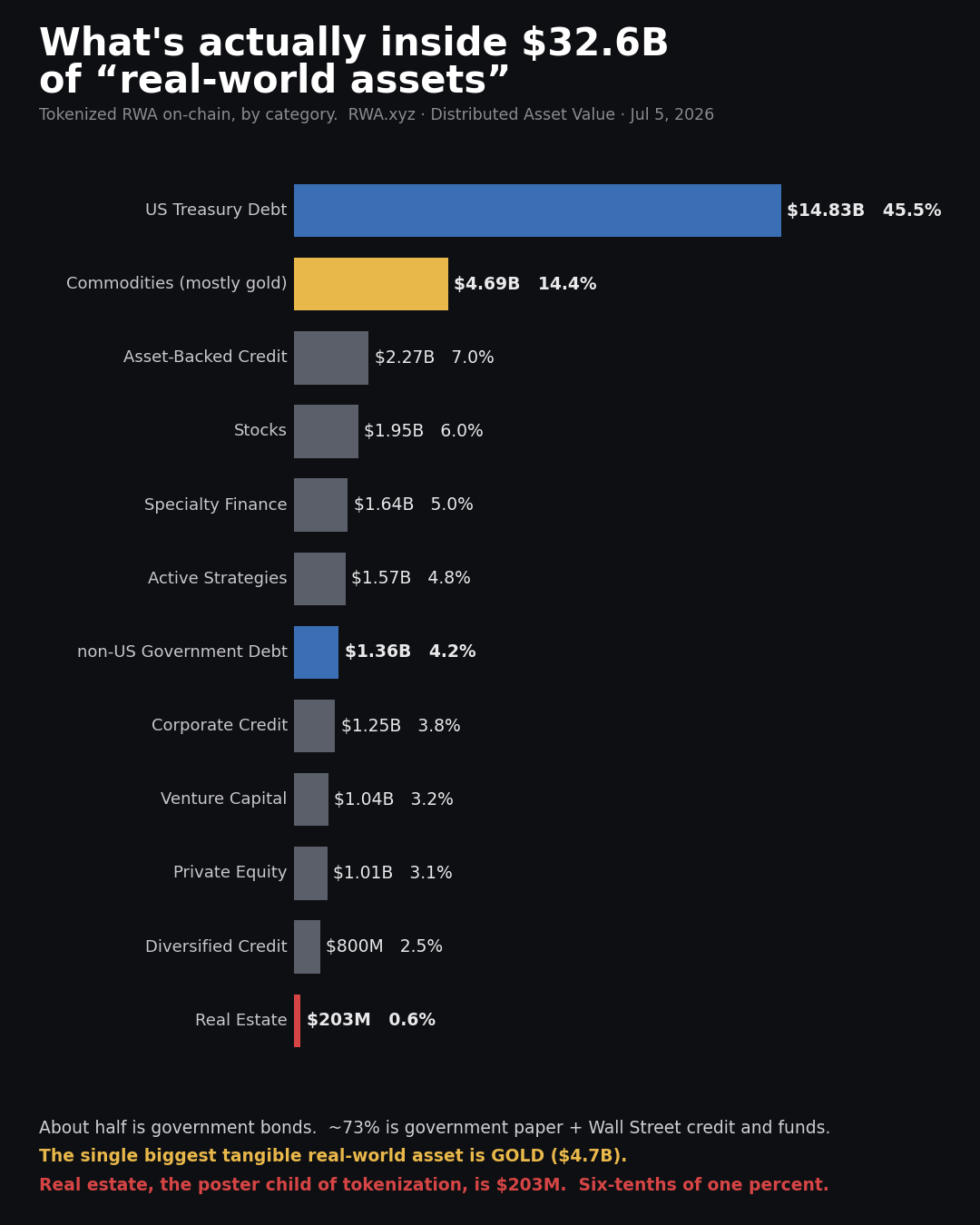

Here is the full composition of the on-chain RWA total as of July 5 2026, largest category first. The percentages are share of the roughly $32.62 billion total. Verify current, because the mix shifts as new issuance lands.

| Category | What it actually is | Value | Share |

|---|---|---|---|

| US Treasury Debt | Tokenized US government bills and bonds, and money-market funds holding them | $14.83B | 45.5% |

| Commodities | Mostly tokenized gold, plus a little other metal | $4.69B | 14.4% |

| Asset-Backed Credit | On-chain private credit collateralised against loan pools | $2.27B | 7.0% |

| Stocks | Tokenized public equities and equity wrappers | $1.95B | 6.0% |

| Specialty Finance | Niche lending strategies and structured receivables | $1.64B | 5.0% |

| Active Strategies | Actively managed on-chain funds and yield strategies | $1.57B | 4.8% |

| Non-US Government Debt | Tokenized sovereign debt outside the US | $1.36B | 4.2% |

| Corporate Credit | Tokenized corporate lending and bonds | $1.25B | 3.8% |

| Venture Capital | Tokenized venture fund interests | $1.04B | 3.2% |

| Private Equity | Tokenized private-equity fund interests | $1.01B | 3.1% |

| Diversified Credit | Mixed on-chain credit portfolios | $0.80B | 2.5% |

| Real Estate | Tokenized property and property-backed instruments | $0.20B | 0.6% |

| Total | On-chain distributed asset value | $32.62B | 100% |

A note on the arithmetic, because honesty about the number is the whole point of this page. Each category above is rounded on its own, so the twelve components add to about the total rather than to it exactly. The rounded parts sum to roughly $32.61 billion, which reconciles to the stated $32.62 billion once you carry the unrounded figures. No line is inflated to make the total look bigger, and the total is not padded to make a line look smaller. What you see is the real composition, rounded honestly.