Stellar just crossed $200 million in DeFi TVL for the first time. The crypto press ran it like a coronation. Blockonomi called it a “record milestone driven by RWA tokenization and institutional capital flows.” Analysts talked about structural shifts, Soroban’s smart contract platform, and institutional investors deploying serious capital.

I pulled up the numbers. They tell a different story.

I have reviewed over 200 tokenized asset projects in the last three years. This is everything I found on Stellar’s RWA ecosystem.

The headline number

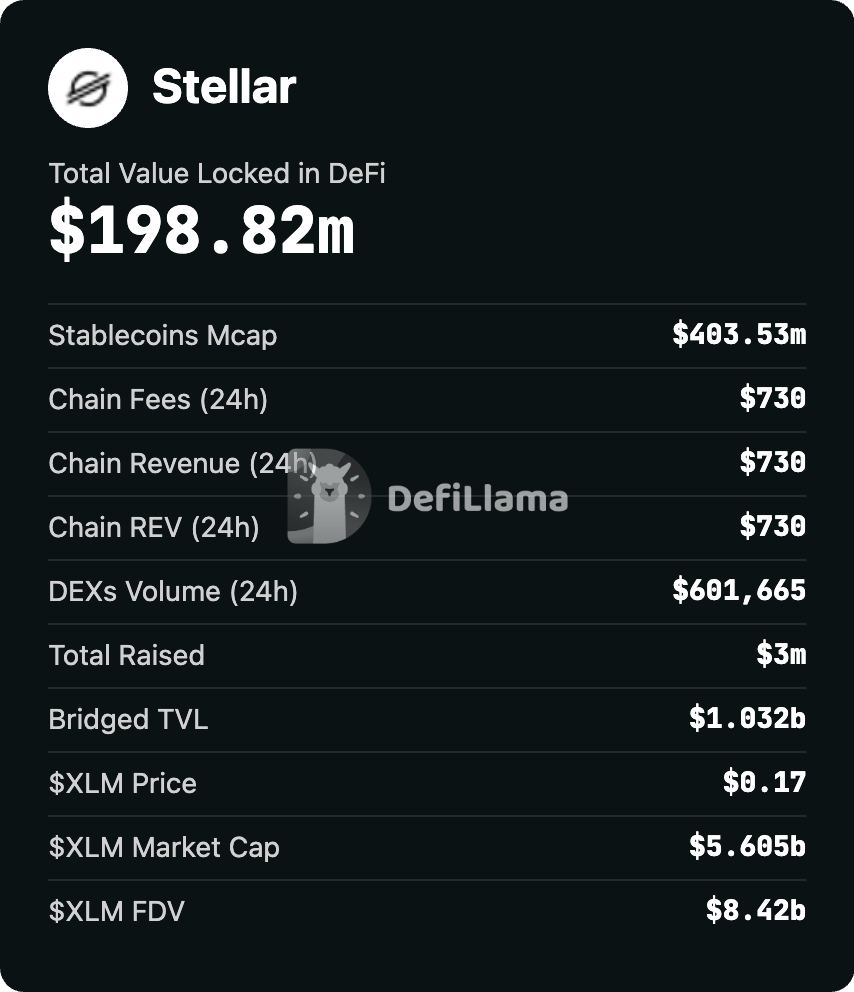

$200 million in DeFi TVL. DefiLlama confirms $198.5 million as of this writing.

But context matters. Ethereum’s DeFi TVL is $45.3 billion. Solana’s is $5.5 billion. Base has $4.4 billion. Arbitrum has $1.7 billion. Even Avalanche, which nobody has talked about in months, has $642 million.

Stellar is celebrating a number that would be a rounding error on Ethereum. It would not make the top ten protocols on Solana.

To be fair, TVL is not the only measure. Stellar has a different story to tell. Let me hear it.

What Stellar actually has

The RWA narrative is not entirely fiction. Actual institutions are issuing tokenized products on Stellar. That part checks out.

Franklin Templeton runs the BENJI/FOBXX fund on Stellar. $637.9 million in tokenized US government money market instruments. This is the same fund that has been on Stellar since 2021. Franklin Templeton chose Stellar early because of low fees and fast settlement. They once reported cutting recordkeeping costs from $50,000 per 50,000 transactions to $120. Hard to argue with that.

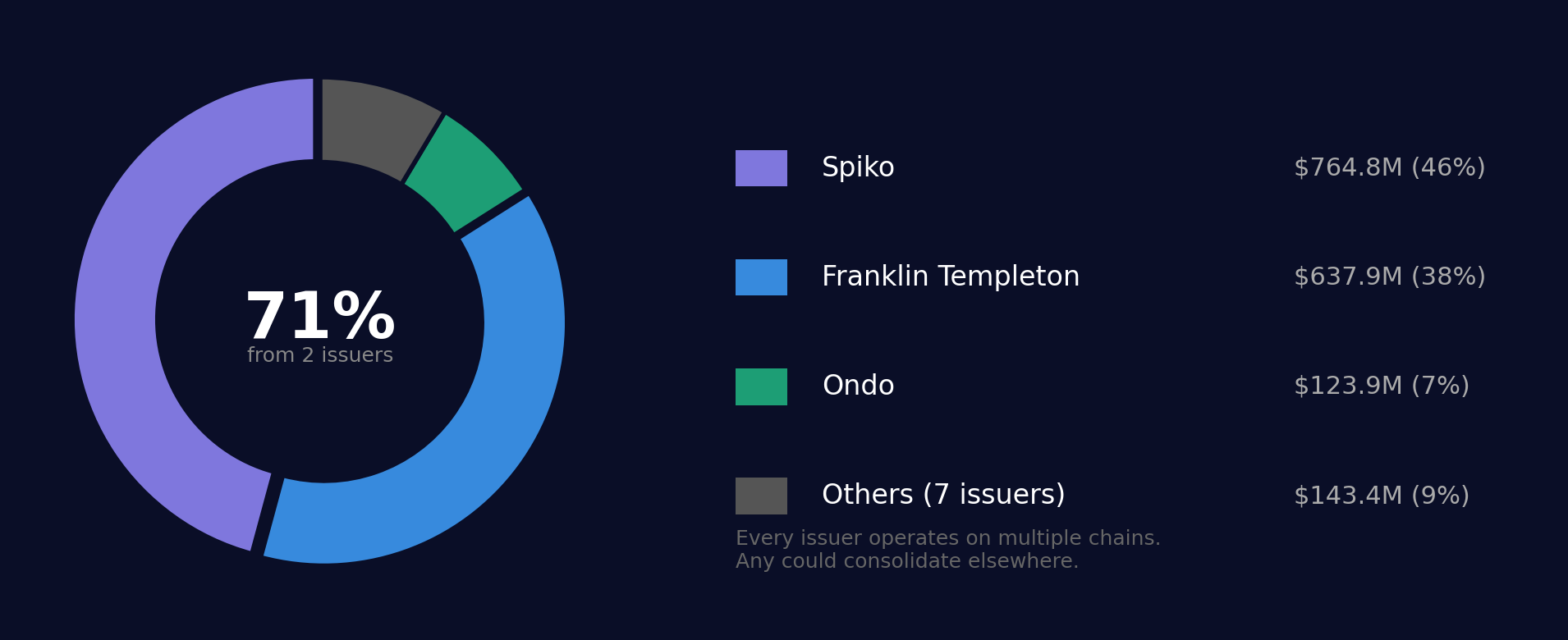

Spiko is the biggest issuer by value: $764.8 million in tokenized European money market funds. Regulated, institutional, boring in the best sense.

Ondo has $123.9 million on Stellar via USDY. WisdomTree has 13 digital funds accessible through WisdomTree Prime, built on Stellar wallets, showing $24 million on DefiLlama.

Add Etherfuse ($4 million in Mexican CETES bonds), Defa by InvoiceMate ($4.9 million in invoice factoring), and VNX ($8.3 million in Euro/CHF stablecoins), and you get a legitimate institutional footprint.

RWA.xyz reports $1.67 billion in distributed asset value on Stellar across 62 assets from 10 issuers. Not a small number. So why am I writing a roast?

Because of everything else.

The numbers nobody mentions

Four numbers.

Market cap: $5.6 billion. Rank #21 on CoinGecko. FDV: $8.42 billion. Stellar is valued like a major infrastructure network.

Daily fees: $730. Not $730 thousand. Not $730 million. Seven hundred and thirty dollars. On a good day it touches $1,800. Annualised, that is roughly $362,000 a year.

DEX volume: $573,000 per day. Across all decentralised exchanges on Stellar. Two protocols account for nearly all of it: Aquarius ($476K) and LumenSwap ($125K). Everything else rounds to zero.

RWA holders: 9,676. Across the entire network. $1.67 billion in tokenised assets held by fewer than 10,000 addresses.

Now do the math.

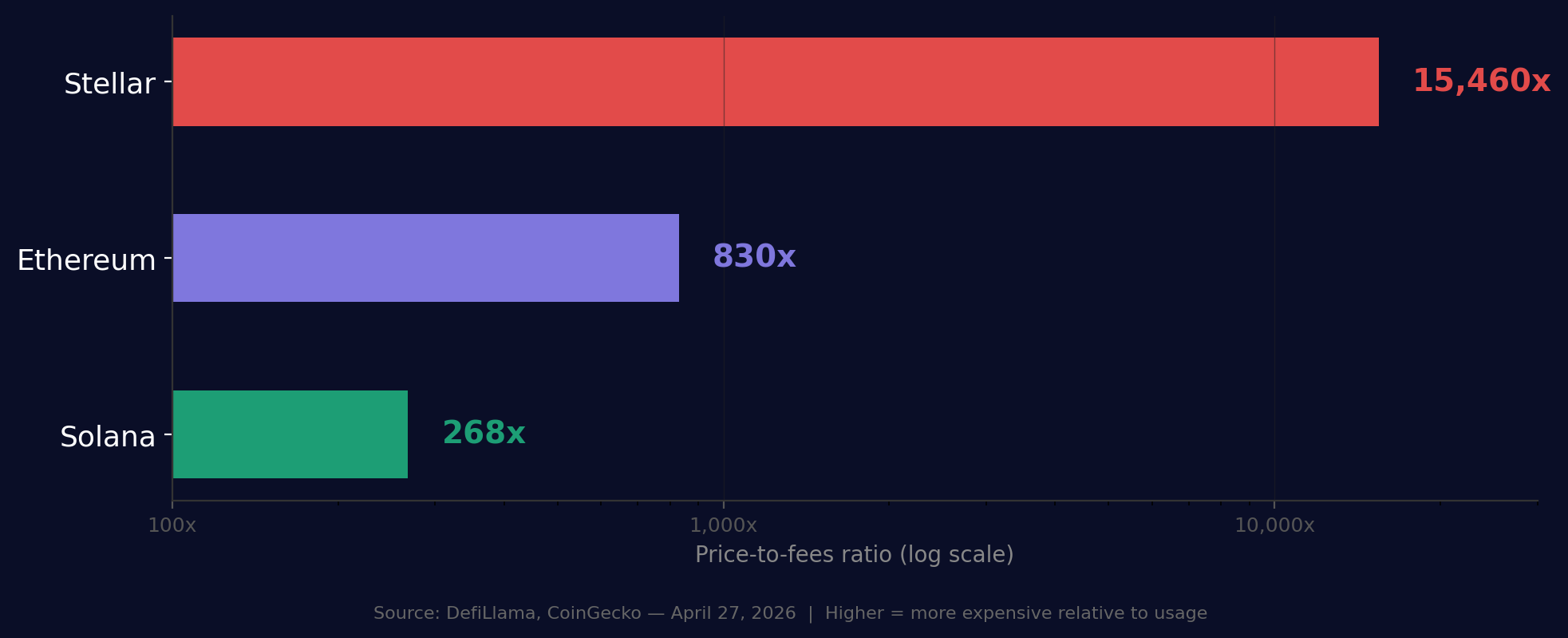

$5.6 billion market cap divided by $362,000 in annual fees = a P/E ratio of 15,460.

For context, using the same source (DefiLlama) and the same metric: Solana’s current P/Fees ratio is around 268. Ethereum’s is around 830 after fee compression post-Dencun. Both of those numbers are already stretched by traditional standards. Stellar is at 15,460.

A food truck in a mid-tier American city generates more annual revenue than the entire Stellar network.

The two-issuer problem

Seventy-one percent of all RWA value on Stellar comes from two issuers: Spiko and Franklin Templeton.

Two entities propping up an entire chain’s narrative. Both of them could move to Ethereum tomorrow.

If Franklin Templeton decides to consolidate its tokenisation efforts on Ethereum (where it also operates), or if Spiko expands to Polygon or Base, Stellar’s RWA narrative loses more than half its substance overnight.

Every one of these issuers operates on multiple chains. Ondo has $2.74 billion in total TVL but only $123.9 million on Stellar. WisdomTree has $869 million total but $24 million on Stellar. Franklin Templeton runs on Ethereum, Polygon, and Stellar simultaneously.

Stellar is not the home for RWA tokenisation. It is one of several addresses. And it is not the biggest one.

The TVL vs. activity gap

RWA.xyz reports $1.67 billion in tokenised assets on Stellar. DefiLlama reports $198 million in DeFi TVL.

So where is the other $1.47 billion?

It is sitting there. The tokens exist on a ledger, accounted for, doing very little. Almost nobody trades them. I could not find meaningful collateral usage or yield strategies built on top of them. The 30-day transfer volume for all RWA assets on Stellar is $124 million, which means monthly turnover on $1.67 billion worth of assets is 7.4%.

These are ledger entries, not active financial instruments.

The DeFi ecosystem that supposedly benefits from all this institutional capital has one lending protocol worth mentioning (Blend at $106.7 million) and a handful of DEXs that collectively process less volume per day than a single mid-tier Uniswap pool on Ethereum.

Soroban, Stellar’s smart contract platform that was supposed to unlock all of this, launched over two years ago with a $100 million adoption fund. It supported 160 projects. The results: Soroswap ($1.2 million TVL), Phoenix DeFi Hub ($1.5 million), FxDAO ($45,000), DeFindex ($1 million). The network still limits smart contract transactions to 100 per ledger.

$100 million spent. 160 projects funded. $45,000 in TVL in one of the resulting protocols.

The payments legacy

Stellar was never built to compete with Ethereum’s DeFi stack. It was designed for cross-border payments and asset transfers. And in that specific lane, it has legitimate advantages: low fees, fast finality, and a network of anchor institutions that process real-world payments.

Franklin Templeton did not choose Stellar for its DeFi ecosystem. They chose it for cost efficiency and settlement speed. And that advantage has nothing to do with TVL or DEX volume.

The question is whether that value proposition justifies a $5.6 billion market cap when the chain generates less than $1,000 a day in fees.

The same four questions

I apply the same framework to every RWA project I review.

What is the yield, and where does it come from?

On the RWA side, the yield is real. Franklin Templeton’s FOBXX pays Treasury yields. Spiko’s money market funds pay institutional rates. Ondo’s USDY pays 3.55%. The yield comes from government bonds and money markets. The income is sourced from regulated instruments, not from token emissions or protocol-subsidised returns. Clean.

What do you actually own?

The tokenised assets represent actual claims on registered instruments. FOBXX holders own shares of a registered fund. The token is a wrapper for a real-world claim, not a governance share standing on its own. No issues here.

Can you exit?

Through the issuer, yes. Through secondary markets on Stellar? With $573,000 in daily DEX volume, your exit depends on the issuer’s redemption process, not the market. For anything above a few thousand dollars, you are not trading out. You are requesting a withdrawal. This is where it gets thin.

Is there skin in the game?

The issuers have skin in the game. Franklin Templeton is a $1.5 trillion AUM firm. Spiko is regulated in Europe. Ondo is backed by Pantera and Founders Fund. But Stellar itself, the chain, the XLM token, has no mechanism that ties token value to ecosystem activity. $730 a day in fees flowing through a $5.6 billion network is not skin in the game. It is decoration.

Franklin Templeton, Spiko, Ondo, and WisdomTree are serious financial institutions with serious products on Stellar. I am not questioning them. I am questioning the chain wrapping those products.

It is valued at $5.6 billion while generating $362,000 a year in fees. The DeFi ecosystem barely exists. The DEX volume would not sustain a single market maker. And the smart contract platform has had two years, $100 million in funding, and produced $45,000 in TVL in one of its featured protocols.

Real assets exist on Stellar. The $5.6 billion price tag around them is the problem. If you are evaluating XLM as an investment based on the “institutional RWA adoption” thesis, look at the numbers behind the narrative. The products are legitimate. The valuation is the issue.

Sources

- DefiLlama: Stellar Chain TVL, fees, DEX volumes (live data, April 27, 2026)

- CoinGecko: XLM market cap, FDV, circulating supply (live data, April 27, 2026)

- RWA.xyz: Stellar network distributed asset value, issuer breakdown, holder count

- Blockonomi: “Stellar DeFi Hits $200M TVL” (April 26, 2026)

- Franklin Templeton: FOBXX recordkeeping cost reduction case study

- Stellar Foundation: Soroban roadmap, Protocol 25 upgrade schedule

- CryptoAdventure: Stellar XLM Review 2026

This is the fourth in a series where I take a real project and run the same due diligence I would use before putting my own money in. To get the next one first, join the Telegram or follow me on LinkedIn.

Nothing in this article is investment advice. I have no position in XLM. I review tokenised asset projects because most of them do not survive first contact with the spreadsheet.